Is Travel Hacking Basically Prepaid Discount Travel?

Earlier this year, I had a dream about being in an apocalypse world. Above the heavily torn urban landscape, flying demons lurked about in the sky and occasionally dived down hunting for human flesh. Streets were filled with dead people scattering in concrete rubble. Back “home” in a barely standing walk-up, my landlord was making a fellow tenant cut off his finger for being three days late on rent payment. I was unfazed. Strolling past countless destruction, I entered a Fidelity branch in an unmarked building and asked about depositing $50,000 in exchange for 25,000 United or American miles. As I debated between the choices, the representative handed me a duct-taped plastic bomb set to detonate at the deadline for my deposit.

It’s all about priorities.

I woke up to the realization that none of it was real, except my plan to deposit $50k with Fidelity for miles. Then it dawned on me that points & miles were no longer just a hobby… it had become a serious obsession. Moving large sums of money around for airline miles, paying credit card fees, and hoarding gift cards are all convoluted activities that come with a cost. I could not have imagined myself doing any of this before starting to play this points & miles game, .

I figured I needed to take a holistic view of this game. How much am I spending on points & miles? Is it worth it? It’s time for a cost-benefit analysis.

COST

During the twelve-month period from July 2016 through June 2017, my wife and I collectively spent $8,729 in this game. Here’s the breakdown:

$3,720 in annual fees:

- $1,909 were paid in order to earn sign-on bonuses

- $800 were paid for the Citi Prestige and Chase Sapphire Reserve that we intended to keep long-term

- $178 were in order to earn the annual spend/retention bonus on AA Aviator cards

- $493 were for the annual free night and points from hotel cards (Hyatt, IHG, Marriott, and Club Carlson)

- $340 were to keep several Amex cards around just in case great Amex Offers come along

$713 in manufactured spending (MS) costs. Those $4.95 VISA gift card fees and $1.60 money order fees sure add up! Though with the continuous decline in MS opportunities, I’m sure this was significantly lower than the year prior, and will likely drop further in the near future.

$702 in convenience fees. It was great being able to use credit cards to pay federal income tax on pay1040.com, property tax via my county’s tax collection website, and mortgage through Plastiq. However, the fees ranging from 1.87% to 2.50% weren’t cheap! On a standalone basis, it rarely made sense to agree to such high fees; however, these opportunities came in handy when I had multiple sign-on and retention spending requirements.

$3,595 in opportunity costs. If I had put all of my organic and manufactured spending on a 2% cash back card over the past year, I would’ve collected this much in cash rewards. By choose to divert these spends on other credit cards, I was foregoing a full month of Bay Area rent!

Despite being conscious about every credit card I applied for and every swipe made with it, I didn’t fully realize how much we were spending playing this game. Whoa! Now, is it stupid or is it worth something?

I miss those daily trips to Walgreens. But maybe it’s a good thing I can no longer waste money on reload fees.

REWARDS

On the other side of the equation are the rewards that we get back from these expensive credit cards and associated activities. Over the same 12-month period:

$4,768 in statement credits. These are a main reason why we hold on to certain cards. They include cash statement credits for meeting minimum spend, annual travel credits from premium cards, 4th-night-free hotel credits from Citi Prestige, and a variety of spend-based credits via Amex Offers and BankAmeriDeals.

Six nights of hotel via free night certificates. It was great being able to book short stays in Hyatt, IHG, and Marriott properties without any cash outlay. Most of these weren’t fancy properties, but together they still retailed $1,297, a substantial sum that we didn’t have to pay.

1,444,401 points & miles – the main reason we play this game. 64% of them came from sign-on bonuses, 12% were from retention/other bonuses, and the rest were from spend. Note that I did not include sign-on or other bonuses from cards with no annual fees (i.e. Merrill+ or Discover IT Miles). Without a direct or opportunity cost, those are the truly “free” points that are out of scope for this analysis.

It’s difficult to meaningfully value the 1.4 million points that we earned across a dozen programs. Thankfully, we also spent quite a bit and exchanged these virtual currencies for actual travel. Over the same 12-month period, we paid 769,641 points for premium flights, economy flights, and hotel nights totaling $19,438 in face value. A simple pro-ration to the remaining 674,760 points yields a potential face value of $17,042 in travel.

And there’s Priority Pass membership. Unlimited access for my wife and I, if purchased directly, costs $798 a year…

Combining the above, in just twelve months, our credit card game generated a face value of $43,343 in statement credits and travel! That’s huge!

Now, of course, let’s not take things at face value. If I never plan on paying $3,500 in cash for a business class flight, then the same flight on miles isn’t really worth $3,500. Travel credits that are tied to specific airline purchases may be worth 90 cents on a dollar. Amex Offers are worth far less if they sway me to buy things that I otherwise wouldn’t. The rigid constraints around 4th-night-free and free night certificates are detrimental to the experience, and one must not forget to account for the lack of points earning on award travel. Priority Pass? I might be willingly pay $100.

I went through my records and assigned a “gut feeling” value on every statement credit, hotel night, and flight. With this non-scientific approach, my valuation of these rewards drops nearly half to $23,820.

The sixth Priority Pass membership has a marginal value of $0.

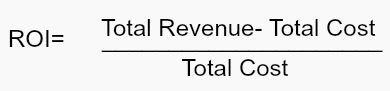

RETURN ON INVESTMENT

Per Econ 101, here’s the equation for return on investment:

At face value, my ROI is ($43,343-$8,729)/$8,729 = 397%. With my valuation, it drops to ($23,820-$8,729)/$8,729 = 173%.

I don’t know about you, but even the low end of that range beats any of my bank accounts, stocks, or real estate by a whole order of magnitude. This exercise confirms that despite the eyebrow-raising cost, this game with multiple of $450 annual fees is still more than worthwhile.

Not factored here is the time value of money. I’d guesstimate that most points I earn sit there for at least two years before being used. Also, I’ve been earning twice as much rewards as I used them. Not a big deal in the grand scheme of things, but the risks of devaluation and shut-down do suppress the value of my savings in these currencies.

Also not factored here is the value of labor. I spend way more time reading about reward programs, paying credit card bills, and calling banks than most of my friends can imagine. I happily do it as a hobby. However, even if I had paid myself a fair wage for this work ($25 per hour?), the ROI would’ve remained strong.

CONCLUSIONS

I began playing the credit card game on the promises of “free premium travel”. That turned out misleading – that even before we get to pay the redemption fees and fuel surcharges for an award flight, various credit card fees and opportunity costs have to be invested. We end up prepaying a not insignificant amount – in my case slightly over 1/3 – of such “free” travel. Far from actually being free, but no doubt it is still an incredible discount.

Do you also see the credit card, points, and miles game as a prepayment for travel?

Nice article on the economics of MS and Churning. As to that dream, some of it actually was real – Gollum identified your flying demons as RATs on Wings (The Two Towers, 2002). Keep your eyes out for those Rewards Abuse Teams…

What abuse? 😉

Yes, absolutely, see it the same way. But I’m also wondering when is enough. However, I can’t help but think that the walmart liquidation option isn’t going to last forever.

Also, where do you buy money orders? My walmart fee is $1.40.

Post office. Wish I had a Walmart nearby, but I don’t.

I love the analysis. I play the game not nearly as hard as you so my ROI is higher, but your absolute amount is higher.

Best thing I read on The “Hobby” all weekend, welcome to TBB!

I think we are all sick, thinking to start a THA group, Travel Hackers Anonymous.

Hi, my name is George and I am addicted to miles 🙂

The end is near…Welcome all the new Rewards Abuse Team at Barclays, sigh.

In many ways, it totally is. Spend $400-$500 on a premium credit card annual fee and get $1000-$2000 in rewards and discounts is a great example of this. But, it is a tradeoff I will do all the time.

What do you use to buy the MO’s?

Post office. The one near home stopped accepting split debit payments, but a few near work are still okay with it. YMMV and I don’t count on being able to do it for much longer.

I know that I’m one year late with my comment 🙂 but damn, that’s unbelievable what’s possible to achieve in States. Here is only one bank in whole country, which have credit card to collect points.